Table of Contents

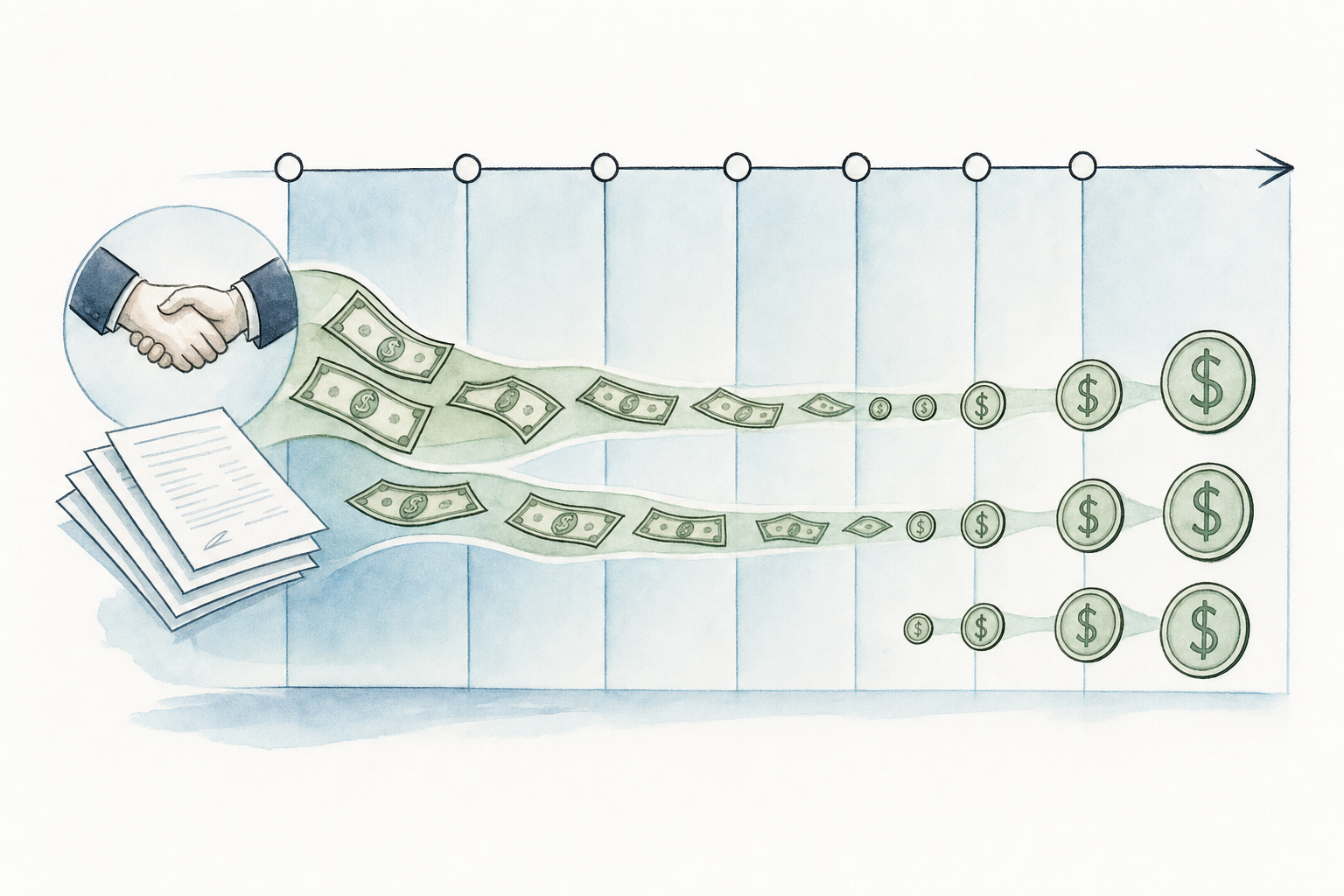

Most businesses track revenue religiously and ignore the collection schedule until cash runs short. Then they scramble to work out why the bank balance doesn't match the sales report. A schedule of expected cash collections fixes that by showing when your credit sales actually turn into usable cash, broken down by how much arrives in month one, month two, and beyond based on real customer payment behaviour.

This guide walks you through it end to end: how the schedule fits into your cash budget, the formula behind it, a worked example with line-by-line numbers, and how to build the whole thing in Excel. We'll also cover the most common mistakes, how customer payment patterns and DSO shape your numbers, and how a working collections system keeps the schedule grounded in reality instead of wishful thinking.

TLDR:

- A schedule of expected cash collections maps when credit sales actually turn into cash, feeding directly into your cash budget to show real liquidity period by period.

- You calculate it by applying collection percentages to each month's credit sales across aging buckets, adding cash sales, and summing the total expected inflows.

- Payment terms in North America average around 43 days, so build your schedule from observed payment behavior instead of stated terms or your projections will consistently overstate cash.

- Common errors include using one blended collection rate for all customers, forgetting bad debt allowances, and treating the schedule as a one-time exercise instead of updating it as actual collections arrive.

- Invoice Butler runs AR collections autonomously across channels without daily team input; one customer collected $300,000+ overdue and cut DSO by 50+ days, closing gaps between projected and actual cash inflows.

What Is a Schedule of Expected Cash Collections?

A schedule of expected cash collections is a financial planning document that maps out exactly when your business expects to receive cash from sales made on credit. It sits inside the broader cash budget as one of its key inputs, translating your sales figures into actual cash timing.

The core idea is straightforward: not all sales convert to cash on the same day. Some customers pay immediately, others pay 30 days later, and a portion may take even longer.

How It Fits Into the Cash Budget

The schedule feeds directly into your cash receipts section, giving you a realistic picture of liquidity week by week or month by month.

The schedule breaks down into three core components: credit sales by period (the sales figure before any cash arrives), collection percentages (how much of each period's sales arrives in month 1, month 2, and beyond), and total expected collections (the actual cash inflow figure used in your cash budget).

How to Calculate Expected Cash Collections: Formula and Step-by-Step Process

The core formula for calculating expected cash collections is straightforward:

Expected Cash Collections = (Cash Sales for the Period) + (Credit Sales Collections by Aging Bucket)

Here is how that breaks down in practice.

Breaking Down the Formula

Most businesses collect credit sales across multiple periods, so you need to account for collection timing by percentage. A typical setup looks like this:

A typical collection pattern might look like this: 40% collected in the month of sale, 35% one month after sale, 20% two months after sale, and 5% written off as uncollectable bad debt.

These percentages come from your historical accounts receivable data. If you are just starting out, industry averages can serve as a reasonable starting point until your own data matures.

Step-by-Step Process

Different collection patterns produce different cash flow results. A conservative pattern (40% month of sale, 35% one month later, 20% two months later, 5% uncollectable) delivers most cash within 60 days with a built-in bad debt buffer. A slow-paying pattern (20% month of sale, 70% one month later, 10% two months later) creates a large lag between sale and cash arrival, concentrating risk in the second month. A fast-paying pattern collects a higher percentage in the month of sale, improving near-term liquidity but requiring strong customer relationships and payment terms enforcement. A mixed customer pattern segments rates for fast payers versus chronic late payers, producing more accurate forecasts at the cost of tracking multiple collection percentages by customer type.

Here are the four steps to prepare a schedule of expected cash collections:

- Pull your sales figures for each period, separating cash sales from credit sales.

- Apply your collection percentages to each month's credit sales across the relevant collection periods.

- Add cash sales directly to the period they occur, since those are collected immediately.

- Sum each column to get your total expected cash collections for each period.

The result feeds directly into your cash budget, giving you the receipts figure you need to determine whether you will have a surplus or shortfall in a given month.

Schedule of Expected Cash Collections Example with Real Numbers

Take a fictional B2B supplier, Meridian Co., preparing its Q2 2026 schedule. Their collection pattern runs like this: 20% of credit sales are collected in the month of sale, 70% the following month, and 10% two months later. Prior months feed into the quarter, so February ($80,000) and March ($100,000) both roll forward.

Here is how the schedule works out across April, May, and June:

| Collection Source | April | May | June |

|---|---|---|---|

| Current month sales (20%) | $24,000 | $26,000 | $22,000 |

| Prior month sales (70%) | $70,000 | $84,000 | $91,000 |

| Two months prior (10%) | $8,000 | $10,000 | $12,000 |

| Total Expected Collections | $102,000 | $120,000 | $125,000 |

April's $120,000 in sales doesn't fully land until June. That's the lag that catches businesses off guard when they read their revenue figures and assume the cash is already there.

"Revenue tells you what you sold. The collections schedule tells you when you can actually spend it."

The Role of Expected Cash Collections in the Master Budget

The schedule of expected cash collections sits inside a larger document called the master budget, which ties together all of a company's day-to-day and financial plans for a period. Within that structure, the cash collections schedule feeds directly into the cash budget, telling it how much money will actually arrive in the bank each month.

The master budget has two broad sides: operating and financial budgets (cash, balance sheet, income statement). The cash collections schedule bridges those two sides, translating the sales budget's revenue figures into real inflows the cash budget can work with.

Here is how that chain of dependence works across four key documents:

- The sales budget sets projected revenue for each period, broken down by product, region, or customer segment as needed.

- The schedule of expected cash collections converts that revenue into actual cash arrivals by applying collection timing assumptions, such as what percentage of sales are collected in the same month versus the next.

- The cash budget absorbs those inflow figures alongside disbursement data to show net cash position each period.

- The budgeted balance sheet and income statement then reflect the final picture, with accounts receivable balances tying back to your collections schedule.

If the collections schedule is wrong, every downstream document inherits that error. A sales figure and a cash figure are not the same thing, and this schedule is precisely where that distinction gets resolved.

Cash Budget vs. Schedule of Expected Cash Collections: Understanding the Difference

The cash budget covers all cash movements in a period: inflows from collections, loans, and asset sales, plus outflows like payroll, rent, supplier payments, and debt service. The collections schedule is one input into that picture, handling only cash expected from customer sales.

Treating them as synonyms is a common slip. The collections schedule tells you what's coming in from customers. The cash budget tells you whether that's enough to cover everything else.

Common Mistakes When Preparing Cash Collection Schedules

Errors here tend to compound quietly. A miscalculated collection percentage in January can throw off your entire first-quarter cash budget before you even notice. Here are four mistakes worth watching for:

- Assuming all sales collect at the same rate regardless of customer type, seasonality, or payment history. Different customers pay differently, and your collection percentages should reflect that.

- Forgetting uncollectible amounts entirely. If 2% of sales historically go unpaid, that needs to appear in your schedule or your projections will consistently run high.

- Misaligning the timing of collections with the correct sales period. Collections from November credit sales belong in November's row, not December's.

- Treating the schedule as a one-time exercise instead of a rolling document you revisit as actual collections come in.

Key Components of a Cash Collections Schedule: What to Include

Every schedule needs four inputs to function reliably.

- Beginning AR balance, broken out by when each outstanding amount is expected to arrive, beyond the aggregate total owed.

- Current period sales, separated into cash (collected immediately) and credit (collected over future periods).

- Collection pattern assumptions, built from historical payment behavior instead of stated credit terms.

- Bad debt allowances, expressed as a realistic percentage of credit sales based on actual write-off history.

Your terms might say Net 30. Your customers might average 45 days. Build the schedule around what actually happens, because a schedule calibrated to contract language instead of observed behavior will drift from reality fast, and the cash budget downstream will inherit every bit of that drift.

How Customer Payment Patterns Affect Your Collection Schedule

Your stated payment terms are a starting point, not a forecast. In North America, payment terms average around 43 days, and 64% of small businesses carry invoices 60 or more days past due.

That gap is exactly why your collection schedule must be built from observed behavior. Segment customers by how they actually pay: fast payers who clear in 20 days need different percentage assumptions than chronic late payers who routinely push past 60. A single blended rate will overstate early inflows and leave you short on cash at the wrong moment.

Days Sales Outstanding (DSO) and Its Impact on Cash Collections

Days Sales Outstanding (DSO) measures how many days, on average, it takes your business to collect payment after a sale. It sits at the heart of any schedule of expected cash collections because it tells you how far behind your actual cash is from your recorded revenue.

The formula is straightforward: divide your accounts receivable by total credit sales, then multiply by the number of days in the period.

A high DSO means cash is sitting uncollected, which throws off your entire cash budget projection.

Building a Cash Collection Schedule in Excel: Templates and Best Practices

A functional Excel template has a simple structure that makes the schedule repeatable and auditable month after month.

Set up your columns as time periods (Month 1, Month 2, Month 3). Set up rows by sales source, one per originating period, labeled with the sales month and the collection percentage applied. A totals row at the bottom sums all incoming cash for that column.

Here are the core best practices to follow when building your template:

- Lock your collection rate assumptions in a separate input tab so you only update one cell when customer payment behaviour changes, instead of hunting through every formula.

- Use named ranges instead of raw cell references so your SUM formulas stay readable when you audit the sheet six months later.

- Add a variance column beside each period to compare budgeted collections against actual receipts, which is where the real forecasting value lives.

- Colour-code rows by collection lag (current month, 30 days, 60 days) so anyone reviewing the sheet can follow the cash flow story at a glance.

Challenges in Cash Collection That Disrupt Your Schedule

Even the most carefully prepared schedule of expected cash collections can go sideways. Knowing where the friction points live helps you build a more realistic budget from the start.

Here are four common challenges that throw cash collection off course:

- Late payments from customers are the most frequent culprit. When customers pay outside their agreed terms, your actual collections land in a different period than your schedule predicted, creating gaps you have to cover from reserves or credit.

- Bad debt write-offs reduce the collectible portion of your receivables. If your collection percentages assume a lower default rate than reality delivers, your schedule will consistently overstate incoming cash.

- Seasonal demand swings make collection patterns uneven across months. A business with strong Q4 sales may see inflated projected collections in Q1, only to find customers are slower to pay after the holiday rush.

- Disputed invoices stall collections entirely. A single billing disagreement can hold up payment on a large account for weeks, pulling cash out of the expected period.

How Invoice Butler Automates the Collections Process Behind Your Cash Schedule

A cash collection schedule tells you what should arrive. Invoice Butler makes sure it actually does. The service runs collections autonomously across email, phone, Slack, LinkedIn, and supplier portals, handling every follow-up without your team lifting a finger each day.

One customer collected $300,000+ and cut DSO 50+ days after implementing Invoice Butler. Fewer slow-paying accounts means fewer gaps between your projected and actual cash inflows, which is the whole point of building the schedule in the first place.

The reporting goes a layer deeper than most schedules ever do. Invoice Butler tracks when each customer actually promises to pay, so your view of upcoming collections reflects real commitments instead of generic aging assumptions. You can sort and filter your receivables by whatever cut matters that week (overdue bucket, customer, expected pay date) to see exactly which cash is landing when. And if you want those numbers inside your own spreadsheet or budget model, our API lets you pull collections data programmatically, including straight through Claude, so your schedule stays fed with live figures instead of last month's snapshot.

Final Thoughts on Your Cash Collections Forecast

The schedule of expected cash collections bridges the gap between sales and liquidity, but only if the assumptions inside it match real customer behavior. Too many businesses project cash based on credit terms while their customers routinely pay 30 or 60 days late, which makes the whole budget unreliable. Build your schedule around what actually happens, not what the invoice says. If late payments are throwing your collections off schedule every month, see how Invoice Butler keeps cash flowing in without your team sending another reminder email.

FAQ

How do you calculate cash collections from accounts receivable each month?

Multiply each period's credit sales by your collection percentages for the corresponding aging bucket. For example, if you collect 40% in the month of sale, 35% the next month, and 20% two months later, apply those percentages to the respective months' sales figures and sum the totals. Add any cash sales directly to get your total expected collections for that period.

Schedule of expected cash collections vs. cash budget?

The schedule of expected cash collections shows only the cash coming in from customer sales. The cash budget is the complete picture: all inflows (collections, loans, asset sales) and all outflows (payroll, rent, supplier payments, debt service). The collections schedule is one input feeding into the broader cash budget.

What's the fastest way to prepare a schedule of expected cash collections?

Build a reusable Excel template with columns for each time period and rows for sales by month with collection percentages applied. Lock your collection rate assumptions in a separate input tab so you only update one cell when customer payment behavior changes. Most teams complete their first working schedule in under an hour once they have historical AR data to set realistic collection percentages.

How do late payments affect your cash collection schedule?

When customers pay outside their agreed terms, your actual cash arrives in a different period than your schedule predicted, creating gaps you need to cover from reserves or credit. A schedule built on stated payment terms (Net 30) will consistently overestimate early cash if your customers actually average 45 or 60 days to pay. Build the schedule around observed payment behavior, not contract language.

Can Invoice Butler improve the accuracy of my collections schedule?

Yes. The service runs collections autonomously across email, phone, Slack, LinkedIn, and supplier portals, reducing the lag between when invoices are due and when cash actually arrives. One customer cut DSO by more than 50 days after implementing Invoice Butler, which means fewer gaps between projected and actual cash inflows in your schedule.collected $300,000+ and cut DSO 50+ days