"Approved" isn't paid until banking clears.

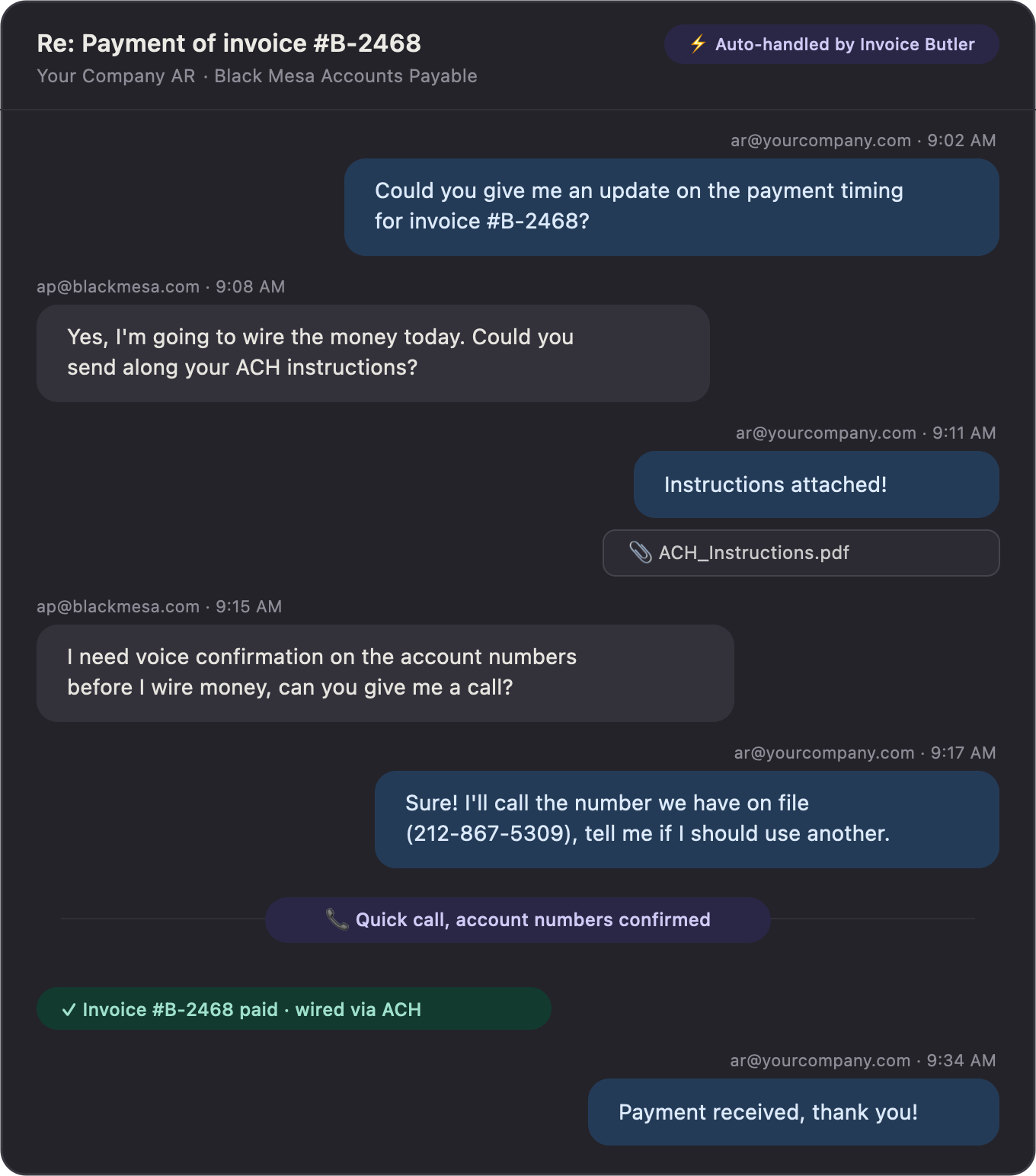

Verification forms, penny tests, callback confirmations, portal banking modules, the last mile between an approved invoice and money in your account. Invoice Butler runs it all, so payment-ready means actually ready.

The invisible step that quietly holds your cash.

Your invoice is approved. The payment run is scheduled. And then nothing arrives, because somewhere in your customer's AP process, your banking details are sitting unverified. Maybe a verification form went to a defunct alias. Maybe their fraud-prevention policy requires a callback no one picked up. Maybe the portal's banking module wants a voided check uploaded in a format nobody mentioned. You find out when the payment doesn't land.

This step exists for good reason, vendor fraud and ACH redirection scams are real, and every serious AP team now verifies banking changes out-of-band. But it makes verification a process two companies share and neither owns. Your reminder software has no idea this step exists; it's still emailing "just following up!" about an invoice that's approved, scheduled, and physically unable to pay out.

And it recurs: every new enterprise customer, every banking change, every portal migration re-triggers it. For a lean team, it's death by paperwork, five different verification procedures for five different customers, each one "just a quick form" that costs a week of float when it slips.

Payment-readiness, treated as the collections work it is.

Invoice Butler owns the banking verification step end to end. It detects when verification is the actual blocker, completes each customer's procedure, forms, portal banking modules, micro-deposit confirmations, and makes sure callback verifications actually connect with a real person available on your side of the process. Every requirement is tracked to completion, so invoices enter payment runs able to pay. When your banking ever changes, the butler re-verifies across every customer before the change can strand a single payment.

What the Butler handles

Blocker detection

"Approved but unpaid" gets diagnosed, not re-reminded. If banking verification is the holdup, that's what gets worked.

Forms and portals, completed

Bank letters, voided checks, vendor banking modules in Coupa, Ariba, Tipalti — filled, formatted, submitted.

Callback coordination

Out-of-band verification calls scheduled and confirmed with a designated, pre-briefed person on your team. No more phone tag with a fraud-prevention desk.

Micro-deposit handling

Penny tests tracked and confirmed on time, so a two-cent transaction never delays a six-figure payment.

Payment-readiness tracking

A per-customer readiness status: verified, pending, blocked — visible before invoices age, not after.

Change management

New bank account? The butler re-runs verification with every active customer, sequenced so no payment run gets missed.

Live in under a week

Readiness gets mapped

The butler inventories which customers have verified banking and which are silently blocked. Most teams find surprises on day one.

Each procedure gets worked

Forms, portal modules, penny tests, and callback scheduling — executed per each customer's specific process.

Humans handle the calls

When a customer's bank-change desk needs a voice, verification calls are coordinated with your designated approver, briefed and ready.

Readiness stays current

Status tracked continuously; any banking change on either side triggers re-verification before it can cost a payment cycle.

Know who can actually pay you, before the payment run.

The step nobody owned, now owned.

Late payments happen because no one has time to consistently move them forward. We do, handling the full collections cycle, not just the first email.

Greptile's one-person ops/finance team was losing $12K+ every 60 days to failed and stalled payments, $70K+ annualized, until the butler took over payment-readiness and retries.

Common questions

Why is banking verification a collections problem?

Because it delays cash exactly like an unpaid invoice does — an approved invoice blocked on verification is unpaid revenue with extra steps. Anything between invoice sent and cash received is collections, whether or not it looks like dunning.

Can't our customers just verify us once?

Each customer verifies independently, by their own procedure, and re-verifies on any banking change. With 50 enterprise customers, that's 50 separate processes — which is why it needs an owner, not a reminder.

How do callback verifications work if they need someone from our company?

The butler schedules the call, briefs your designated approver on exactly what will be asked, confirms the appointment with the customer's verification desk, and follows up if it's missed. Your person spends five minutes; the butler spends the rest.

Is this secure? You're handling our banking details.

Invoice Butler is SOC 2 Type 1 and Type 2 certified, and banking data is handled under those controls end to end. Documentation available via security@invoicebutler.ai.

Does this overlap with the W-9 and vendor onboarding work?

They're siblings — banking verification, W-9s and tax forms, and portal onboarding usually arrive together when a new enterprise customer sets you up as a vendor. The butler runs all three as one onboarding motion.

What happens when we change banks?

Tell the butler once. It sequences re-verification across every active customer — prioritized by upcoming payment runs — so the transition doesn't strand a single payment.

Find the approved invoices that can't pay you.

A 30-minute demo includes a look at where payment-readiness typically leaks.

Book a demo