Table of Contents

The formula for DSO takes about ten seconds to learn and a few months to use correctly. You plug in your accounts receivable and credit sales, multiply by your period days, and get a number that might mean absolutely nothing if you've mixed in cash sales or tried to use the simple method during your busy season. What matters goes beyond the calculation: choosing between the simple and countback methods, setting up your Excel tracker to catch trends before they become problems, and knowing whether your 45-day DSO is actually healthy or hiding a collections issue.

TLDR:

- DSO formula is (Accounts Receivable / Total Credit Sales) × Number of Days

- Compare your DSO against payment terms, not industry averages: 45 days is poor with Net 15 terms

- Use countback method instead of simple calculation if your sales fluctuate seasonally

- Invoice Butler automates collections to reduce DSO by 50+ days through personalized follow-ups and portal management

What Is Days Sales Outstanding (DSO)

Days Sales Outstanding measures how long it takes your business to collect payment after making a credit sale. Think of it as the gap between when you deliver value to a customer and when cash actually hits your bank account. If you invoice a client today and they pay 45 days later, that's 45 days of DSO.

This metric matters because it directly affects your cash flow health. A high DSO means money sits in accounts receivable instead of your bank account, where you could use it to pay suppliers, invest in growth, or simply keep operations running. When customers take longer to pay, you're essentially providing them with free financing while your own bills pile up.

The DSO Formula Explained

The standard DSO formula looks like this:

DSO = (Accounts Receivable / Total Credit Sales) × Number of Days

Each component serves a specific purpose. Accounts receivable is what customers currently owe you for credit sales. Total credit sales represents revenue you invoiced during the measurement period (cash sales don't create receivables). The number of days is your measurement window, typically 30, 60, 90, or 365 days.

You can use either ending or average accounts receivable. Ending AR is your receivables balance on the period's final day. Average AR adds your beginning and ending balances, then divides by two.

How to Calculate DSO: Step-by-Step Example

Let's walk through a real calculation. Say your company has $50,000 in accounts receivable at month-end, and you generated $150,000 in credit sales during that 30-day period.

Plugging into the formula:

DSO = ($50,000 / $150,000) × 30 days = 10 days

In other words, you collect payment, on average, 10 days after invoicing. That's quite healthy.

For a quarterly calculation, the approach stays the same but the numbers change. If you have $75,000 in AR and $450,000 in credit sales over 90 days:

DSO = ($75,000 / $450,000) × 90 days = 15 days

Annual calculations work identically.

DSO Calculation Methods: Simple vs Countback

The simple method works well when your sales stay consistent month to month. It gives you a snapshot based on current AR and recent sales.

The countback method works backward through your sales history, subtracting each period's sales from your current AR until you hit zero. This tells you exactly which invoicing periods remain unpaid.

When does countback matter? Seasonal businesses or companies with uneven revenue. If you sell £20,000 in January but £200,000 in December, the simple method can mislead you. A large December might make your DSO look artificially low in early January, even if customers pay slowly.

Countback accounts for this by matching receivables to the actual months they came from.

How to Calculate DSO in Excel

Start by setting up your spreadsheet with three columns: Accounts Receivable, Credit Sales, and Days in Period. In a fourth column, create your DSO formula.

If your AR is in cell A2, credit sales in B2, and period days in C2, your formula becomes:

=(A2/B2)*C2

For a monthly tracker, list each month in rows. Put your AR balance in column A, monthly credit sales in column B, and enter 30 (or actual days) in column C. Copy the formula down, and Excel calculates DSO for each month automatically.

To track trends, add a line chart linked to your DSO column. You'll spot problems the moment the line climbs.

Pull your AR and sales figures directly from your accounting system each month. This prevents errors and saves time.

DSO Benchmarks by Industry

DSO varies wildly depending on your industry. What looks terrible for a retailer might be perfectly normal for a manufacturer dealing with complex procurement cycles.

Retail and e-commerce businesses see the lowest numbers because most transactions happen via credit card or immediate payment. Healthcare sits at the opposite end because insurance claims create processing delays.

Your real benchmark isn't a universal standard. Compare your DSO against direct competitors facing the same customer payment behaviors. A 50-day DSO might signal trouble for a SaaS company but indicate tight collections for a construction supplier.

Understanding DPO (Days Payable Outstanding)

While DSO tracks how quickly you collect from customers, DPO flips the perspective. Days Payable Outstanding measures how long you take to pay your suppliers after receiving goods or services.

The DPO formula mirrors DSO's structure:

DPO = (Accounts Payable / Cost of Goods Sold) × Number of Days

A higher DPO means you hold onto cash longer before paying suppliers. But stretch too far and you risk damaging supplier relationships or missing early payment discounts.

The real power comes from managing DSO and DPO together. Collect from customers in 20 days while paying suppliers in 45 days, and you've got 25 days of positive cash flow cushion.

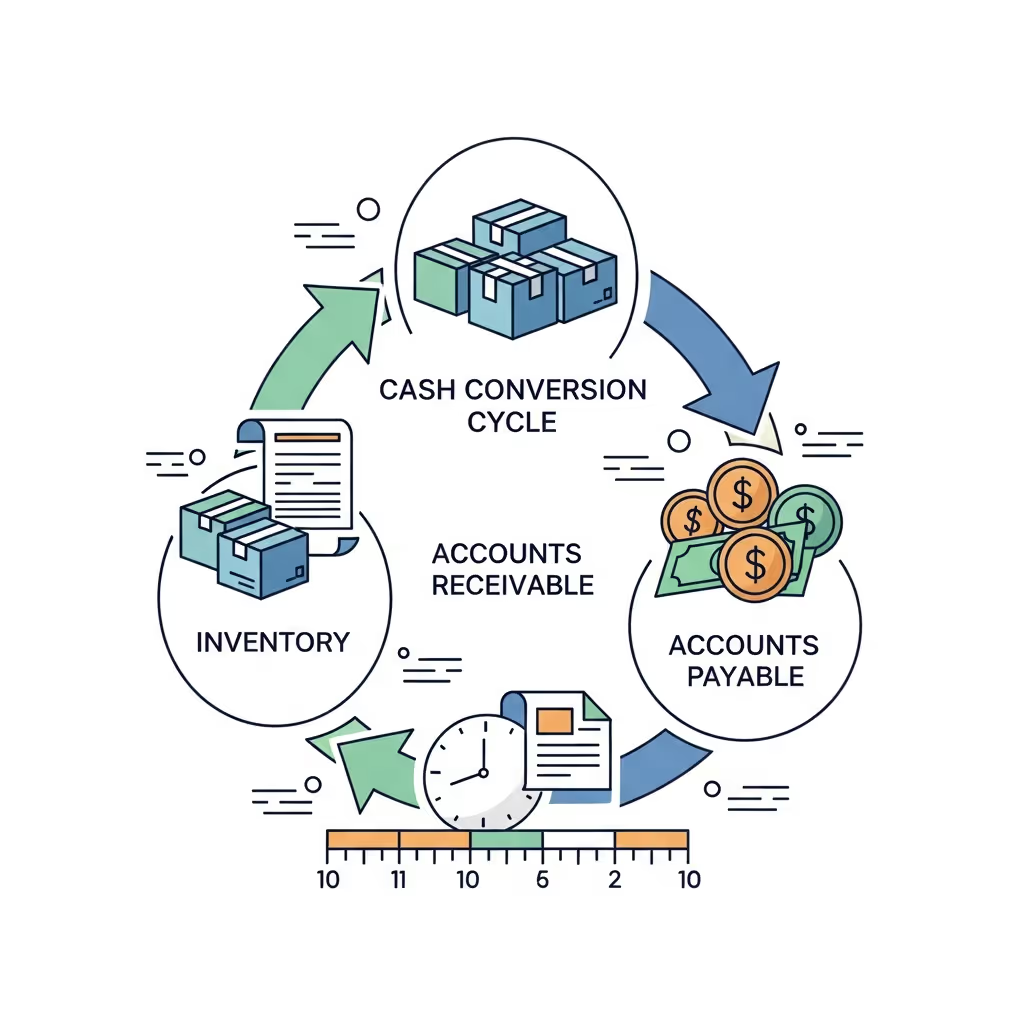

DSO and DPO in the Cash Conversion Cycle

The cash conversion cycle (CCC) connects DSO and DPO to show how long cash remains tied up in operations. The formula is:

CCC = DIO + DSO - DPO

DIO (Days Inventory Outstanding) measures how long inventory sits unsold. Add DSO for collection time, then subtract DPO because paying suppliers later preserves your cash position.

Median cycles run 30 to 45 days. Reducing DSO by 10 days cuts your CCC by 10 days, freeing working capital for reinvestment instead of leaving it locked in receivables.

Why DSO Matters for Cash Flow

Every extra day in your DSO represents cash you can't spend. When receivables stretch from 30 to 45 days, you're floating an additional two weeks of revenue to customers while your own bills don't wait.

This creates real constraints. Payroll hits on the 15th whether customers have paid or not. Suppliers expect payment within their terms, regardless of your collection timeline. Growth opportunities appear when cash is available, not when it's theoretically owed to you.

High DSO forces two uncomfortable positions: draw down credit lines to cover shortfalls, or pass on investments that could grow revenue.

Common Mistakes When Calculating DSO

Judging your DSO without context is the first mistake. A 45-day DSO looks poor if you offer Net 15 terms, but it's quite reasonable if your standard terms are Net 60. Always measure DSO against your actual payment terms to identify genuine collection issues.

Mixing cash and credit sales distorts the calculation. DSO measures how long credit sales take to collect, so including cash transactions (which convert immediately) artificially lowers your number and masks receivables problems.

Seasonal businesses get misleading results when using the simple formula during high or low sales months. Switch to the countback method if your revenue fluctuates month to month.

How to Improve Your DSO

Invoice faster and you get paid faster. Sending invoices immediately after delivery or service completion gives customers the full payment window within your terms. Delayed invoicing cuts into your collection timeline before the clock even starts, which is where invoice follow-up automation tools become helpful.

Review your credit policies if DSO consistently exceeds your payment terms. Are you extending Net 60 to customers who could pay Net 30? Tightening credit terms for new customers or requiring partial upfront payment can trim 10-15 days from collection cycles.

Early payment discounts work when structured properly. Offering 2% off for payment within 10 days gives customers a reason to pay your invoice first. Make payment easy by accepting credit cards, ACH, wire transfers, and digital wallets through multi-channel invoice collections solutions.

Automating DSO Management with Invoice Butler

Calculating DSO tells you where you stand. Actually reducing it requires action on every overdue invoice, and that's where most finance teams hit a wall. Daloopa cut collection times by 50% by taking a systematic approach to this challenge.

Invoice Butler handles the work that drives DSO down. When an invoice goes unpaid, we send personalized follow-ups, respond to customer questions, and track conversations until payment arrives. Beewise collected over $1M in 30 days using this approach with Invoice Butler. If a customer requires supplier portal submissions through Coupa or Ariba, we log in and handle it. When initial contacts don't respond, we find the decision-maker who can authorize payment.

This isn't software you manage. We take the entire collections process off your plate. Clients have cut their DSO by 50+ days and recovered hundreds of thousands in overdue payments, like HotelPORT recovering over $250K in stuck invoices.

Final Thoughts on DSO and Cash Flow Management

The DSO formula in Excel takes minutes to set up and gives you monthly visibility into collection performance. Turning that insight into faster payments is where most finance teams struggle. Your receivables won't collect themselves just because you're tracking them. Focus on sending invoices immediately, following up systematically on overdue accounts, and making payment easy for customers. Watch your DSO trend over time and you'll catch problems early enough to fix them.

FAQ

How often should you calculate DSO?

Calculate DSO monthly to spot trends early. Monthly tracking lets you identify collection problems before they snowball into cash flow crises, and gives you enough data points to see whether your AR performance is improving or deteriorating over time.

What's the difference between simple DSO and countback method?

The simple method divides current AR by recent sales, giving a quick snapshot that works well for steady revenue. The countback method traces backward through your sales history to match receivables to actual invoicing periods, which matters when your revenue fluctuates seasonally or month-to-month.

Can you have a DSO that's too low?

Yes, if it's lower than your payment terms. A 15-day DSO when you offer Net 30 terms might mean you're being too aggressive with collections and potentially damaging customer relationships, or you're not extending credit to qualified buyers who could increase your sales volume.

When should you use average AR instead of ending AR?

Use average AR when your receivables balance swings dramatically during the measurement period. If you invoice heavily at month-start or your customers cluster payments at certain times, averaging your beginning and ending balances smooths out these fluctuations for a more accurate picture.

How do you calculate DSO for just three months?

Take your accounts receivable balance at the end of the quarter, divide by your total credit sales for those 90 days, then multiply by 90. For example: (£75,000 AR / £450,000 sales) × 90 days = 15-day DSO for the quarter.